The Custody Paradox Built trustless. Sold as safe. Regulated as nothing.

What every fintech founder must understand about ownership — before their users find out the hard way.

The assumption

If you deposit assets on a crypto exchange, you own those assets.

This belief underpinned a trillion-dollar industry. It was held by retail investors, institutional allocators, venture funds, and — if their product design is any guide — by many of the founders who built the exchanges themselves. The interfaces said 'your balance.' The marketing said 'your crypto.' Some terms of service even said 'you retain ownership.'

The assumption was structurally false — not in the abstract sense that all financial instruments carry risk, but in a precise legal sense: crypto exchange depositors were not asset owners. They were unsecured creditors. The difference between those two words determines what you recover when a counterparty fails.

You were told you owned it. Legally, you had lent it.

Why Bitcoin was built this way — and what broke

The person who created Bitcoin in 2008 — known only as Satoshi Nakamoto, whose identity has never been established — designed it to solve a specific institutional problem.How do you transfer value between two parties without requiring either to trust a bank, a government, or any central authority?The answer was cryptographic: the private key. Whoever holds the private key controls the asset. No intermediary. No appeal. No counterparty.

This design emerged in the aftermath of the 2008 financial crisis, from a conviction that the trust placed in financial intermediaries — banks, custodians, clearinghouses — had proven catastrophically misplaced. The protocol would replace institutional trust with mathematical certainty.

The architecture was elegant for peer-to-peer settlement. It had one practical limitation: it required both parties to manage their own cryptographic keys. Keys get lost. Inheritance becomes complicated. The cognitive overhead of self-custody at scale is significant. Most people cannot or will not do it.

So exchanges emerged. They offered to hold the keys on behalf of users — providing the usability of a bank account with the speculative upside of a new asset class. This was commercially rational. It was also, precisely, the inversion of the technology's founding logic.

Bitcoin was designed to make intermediaries unnecessary. The intermediaries reappeared within a few years of its launch — and this time without the regulatory architecture, the capital requirements, the fiduciary duties, or the deposit insurance that make intermediaries trustworthy in traditional finance. The exchange layer did not add convenience on top of a trustless system. It replaced the trustless system with a trust-dependent one and called it the same thing.

The legal mechanism: assets versus claims

The distinction between an asset and a claim is not philosophical. It determines recovery.

When you hold shares in a properly structured brokerage account — a securities depot — those shares are your legal property. They sit in a segregated account. They do not appear on the broker's balance sheet. If the broker fails, you receive your shares back. They were never the broker's to lose.

When you deposit cash in a bank, something different happens. The bank takes legal ownership of the cash. You receive a claim against the bank for that amount, backstopped by national deposit insurance schemes up to agreed limits.[7]The distinction is invisible in normal conditions because the accountability infrastructure — capital requirements, regulatory supervision, deposit guarantees, fiduciary law — makes the claim functionally equivalent to ownership. The risk is priced, disclosed, and managed. You have a claim. The claim is well-protected.

Crypto exchange deposits looked like securities custody. They functioned like uninsured cash deposits. In bankruptcy, they were treated as neither. The depositor became a general unsecured creditor — last in line after secured creditors and administrative costs, with no guarantee of recovery and no timeline.

The legal architecture of this outcome was documented precisely. A 2023 analysis in the Texas Law Review argued that retail customer agreements on crypto exchanges systematically failed to create an express trust relationship.[2]The language saying 'you retain ownership' was not language of entrustment. It was marketing copy. In several cases, the terms of service explicitly transferred legal title in deposited assets to the exchange — meaning users had contractually agreed to become unsecured creditors without understanding it.[3]

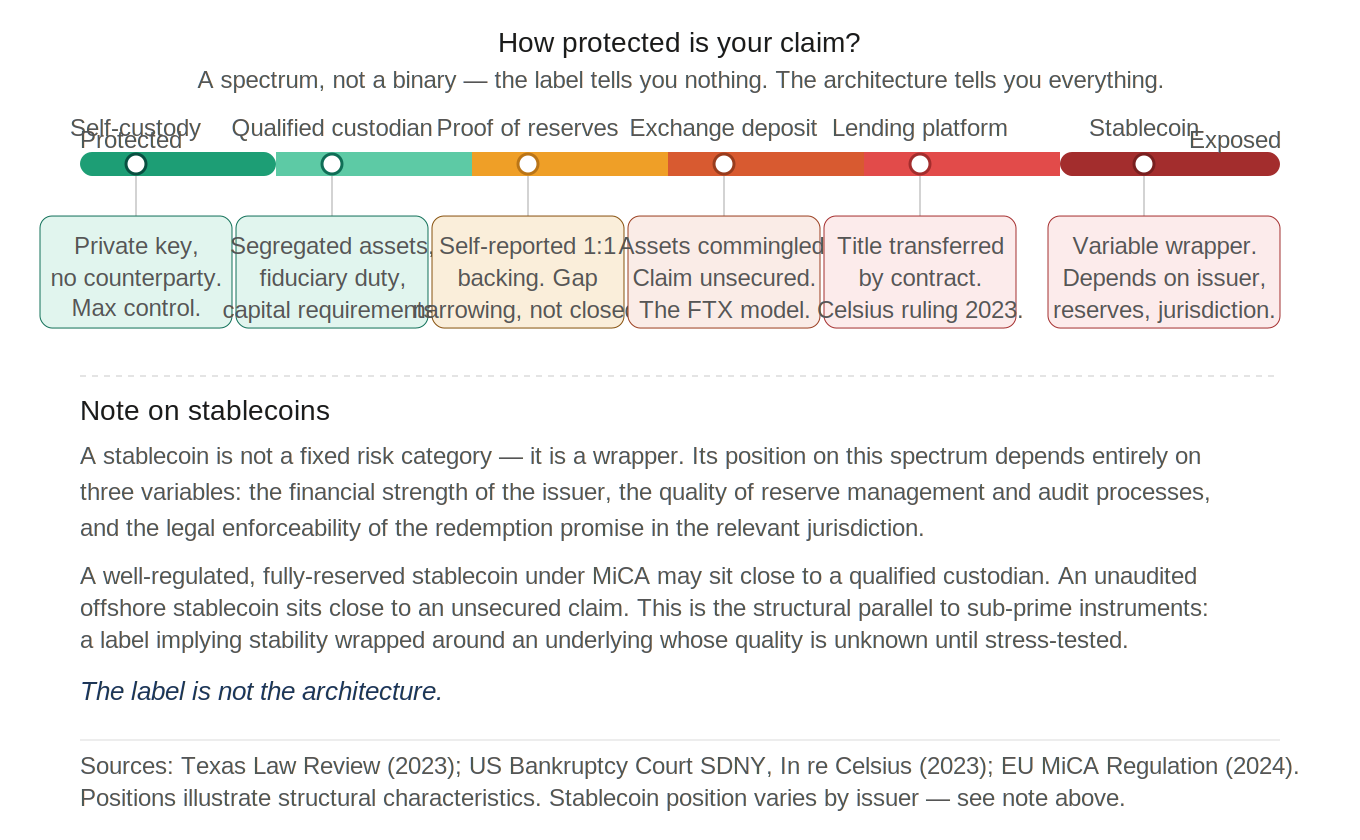

The spectrum below shows that this is not a binary. Protection varies considerably depending on the architecture around the custody relationship.

What this spectrum illustrates is that the word 'claim' covers a wide range of actual protection. Fintech founders building any product where one party holds another party's assets are building somewhere on this spectrum — whether they have mapped that position or not.

The warning that landed in the wrong market

In May 2022, Coinbase disclosed in its SEC 10-Q filing that customer assets could be treated as property of the bankruptcy estate in an insolvency event.[4]Days later, Gary Gensler, then Chair of the US Securities and Exchange Commission (SEC), stated at the FINRA Annual Conference: 'If the platform goes down, guess what? You just have a counterparty relationship with the platform. Get in line in bankruptcy court.'[5]

Gensler was not describing FTX. He was describing the general legal condition of every retail crypto depositor on every centralized exchange. He made this statement in May 2022. FTX collapsed in November 2022.

The gap between the warning and the outcome was not negligence in any dramatic sense. It reflects a structural condition common to emerging markets: the product moved faster than the disclosure infrastructure that normally surrounds financial instruments. Financial media was amplifying the bull narrative rather than interrogating custody law. The traditional finance industry — with its own custody ambiguities and competitive interests — had limited incentive to demand clarity. Retail investors, as in most speculative cycles, were last to understand what they actually held.

The legal reality was available to anyone who read the terms of service carefully. Which is to say, available to almost nobody.

FTX: the most legible proof of concept

FTX did not invent the custody gap. Mt. Gox, which failed in 2014 with the loss of approximately 850,000 Bitcoin, and Celsius, which collapsed alongside FTX in 2022, operated under structurally identical arrangements. What FTX contributed was scale and visibility.

At its peak, FTX was the world's third-largest crypto exchange by volume, with over one million users and a valuation of $32 billion. Its collapse in November 2022 was triggered by a ten-day bank run after a leaked balance sheet revealed that Alameda Research — FTX's affiliated trading firm — held FTX's own native token FTT as its primary collateral. FTT was a token FTX had itself created. When confidence in FTT collapsed, so did the liquidity underpinning both entities.

Sam Bankman-Fried was convicted in November 2023 on seven counts of fraud and sentenced to 25 years. The fraud — which included misappropriation of customer funds for venture investments, real estate, and stadium naming deals — accelerated the collapse and deepened the losses.

But the structure of the failure is worth stating precisely: this was not a rogue actor exploiting a sound system. It was a product built on a legal architecture that offered no protection when tested. The fraud was the stress test. The custody gap was the failure mode it revealed. Without fraud, the commingling of customer and corporate assets, the absence of audits, the self-referential collateral, and the regulatory arbitrage enabled by Bahamas incorporation would still have been present — they would simply have remained invisible for longer.

John Ray III, the restructuring specialist brought in to manage the bankruptcy — the same professional who oversaw the Enron collapse — described what he found as 'a complete failure of corporate controls and a complete absence of trustworthy financial information' unlike anything in his career.

March 31st, 2026: nominal recovery and what it means

Today, the FTX Recovery Trust distributes approximately $2.2 billion to creditors in its fourth round of payments.[8]Several creditor classes reach 100% recovery. Class 7 reaches 120%.

This is a lucky outcome — unusual for a fraud bankruptcy of this scale. It was made possible by two factors: aggressive asset recovery by the insolvency administrators, and the substantial appreciation of crypto assets held by the estate since the November 2022 filing. Without that appreciation, given the scale of the fraud and the misappropriation of customer funds, recovery rates would have been significantly lower. The market, in a sense, bailed out the creditors that the legal architecture had failed to protect.

All payments are calculated at crypto prices from November 11th, 2022 — the date of the bankruptcy filing.[9]Bitcoin traded at approximately $16,871 that day. It subsequently rose above $100,000 and trades near $71,000 today. A creditor whose account held one Bitcoin on the day of the collapse receives dollar recovery equivalent to approximately $16,871 — not to the current value of one Bitcoin.

This is not a criticism of the process, which operated as designed. It is a structural observation: the creditors held claims, and the terms of those claims were fixed at petition date. Whether nominal recovery equals economic recovery depends entirely on what the creditors choose to do with the dollars they receive today — a decision that should have been theirs to make in 2022.

A comparable dynamic appeared in the Lehman Brothers insolvency. Senior creditors eventually recovered close to par, but only after years of illiquidity and complexity that made the nominal outcome a partial picture of the actual loss.

The structural principle: where it applies beyond crypto

The FTX autopsy is a fintech story, but the structural principle extends to any founder building a product where one party defers to another.

Counterparty risk is present in every deferred exchange — any arrangement where value is transferred and a promise of future performance is received in return. The private key is the clearest illustration: the moment you hand it to an exchange, the simultaneous transaction that would make counterparty risk irrelevant has not occurred. You have extended credit. You hold a claim.

What varies across different types of deferred exchange is not whether counterparty risk exists, but whether it is visible, priced, and structurally managed.

For fintech founders specifically, this is a product design question as much as a legal one. Every product involving custody of user assets — payments infrastructure, lending platforms, asset management tools, tokenised instruments — creates a deferred exchange. The thickness of the accountability infrastructure built around that exchange determines whether users hold assets or claims. The interface language does not change the legal reality. A terms of service clause saying 'you retain ownership' is not architecture. It is a sentence.

The same principle extends, at different scales and with different mechanics, to venture investing — where counterparty risk is partially mitigated by skin in the game and alignment of incentives — to supplier relationships where single-source dependencies create undisclosed claims, and to platform dependencies where the terms of service may contain the same structural clause as an FTX user agreement: you retain your data, except when you do not.

In each case the question is identical: does perceived ownership match legal ownership? If not, has the gap been disclosed and priced?

Open questions

—In your own product, where does a user give you something of value and receive a promise in return — rather than an asset? Have you mapped that gap in your terms and your architecture?

—Your product says users 'retain ownership.' What does a court see when it reads that sentence?

—The Celsius Earn account holders transferred legal title to their crypto through a standard terms of service update. Which of your own onboarding or update flows contain a comparable transfer that users have not consciously understood?

—The custody gap at FTX was named publicly by the SEC Chair six months before the collapse. What structural gaps in your own market have already been named — and what has changed as a result?

—Binance now publishes monthly proof of reserves and holds over 20 regulatory licences. Is that sufficient accountability infrastructure to move a depositor from 'unsecured creditor' to 'protected asset owner'? Who decides?

—If the accountability infrastructure around a sovereign currency is itself subject to credit agency revision and debt sustainability questions, what is the right framework for pricing counterparty risk in instruments that sit between sovereign money and crypto custody?

—In your cap table, your supplier contracts, and your platform dependencies — where is there a deferred exchange where nominal value and economic reality diverge? Who holds the claim, and who holds the asset?

Sources and notes

[2]Yadav, M. et al., 'Not Your Keys, Not Your Coins: Unpriced Credit Risk in Cryptocurrency,' Texas Law Review, Vol. 101, 2023. The article demonstrates that retail customers on crypto exchanges hold unsecured credit claims, not asset ownership, and that this risk is systematically unpriced. Available at texaslawreview.org.

[3]Texas Law Review (2023), ibid. The analysis covers standard retail customer agreements across major US exchanges, distinguishing the language of 'ownership' in user interfaces from the legal reality under US bankruptcy law. Separately: American Bar Association, Business Law Today, 'The Crypto Bankruptcy Wave,' March 2023, covering the Celsius ruling (US Bankruptcy Court, SDNY, In re Celsius Network LLC, 2023).

[4]Coinbase Global Inc., Form 10-Q, Q1 2022, filed with the US Securities and Exchange Commission. Reported by Nixon Peabody LLP, 'Hold on for Dear Life,' May 2022.

[5]Gary Gensler, Chair, US Securities and Exchange Commission (SEC), remarks at the FINRA Annual Conference, May 2022. Reported by Loeb & Loeb LLP, 'Get in Line in Bankruptcy Court,' May 2022.

[7]Note on account types: The bank deposit analogy applies to cash accounts, where the bank holds deposits in a creditor-debtor relationship backed by national deposit insurance (FDIC in the US up to $250,000; various EU national schemes). This is categorically different from a securities custody account (stock depot), where shares remain the legal property of the account holder in a segregated account and do not appear on the bank's balance sheet. Crypto exchange deposits functioned legally closer to uninsured cash deposits — with no insurance backstop of any kind.

[8]FTX Recovery Trust, press release, 18 March 2026. Fourth distribution of approximately $2.2 billion on 31 March 2026. Class 5B US customer claims reached 100% cumulative recovery; Class 7 reached 120%. Total distributions since February 2025 approximately $10 billion.

[9]Bitcoin at approximately $16,871 on 11 November 2022 (FTX bankruptcy petition date). Source: CoinDesk market data and FTX Recovery Trust distribution methodology disclosures, which fix claim values at petition-date prices.

Destruction Desk

We perform autopsies on innovation’s failed assumptions.

This newsletter was edited by Manfred Lueth.

You received this email because you signed up for this newsletter from DestructionDesk.com. To stop receiving this newsletter, unsubscribe or manage your email preferences.